Understanding Long Term Care Insurance Options

Overview of Traditional Long Term Care Insurance

Traditional long term care insurance is a well-established option designed specifically to cover long term care needs. It is not intended for short term care or life insurance, although some riders may be available. This type of insurance offers coverage durations ranging from two years to a lifetime.

Key Features and Benefits

- Coverage Duration Options: Policies can range from two years to lifetime coverage.

- Inflation Protection: Most plans include an inflation rider to help benefits keep pace with rising costs.

- Reimbursable Claims: Typically, claims are reimbursed based on actual costs, ensuring that unused benefits remain in the policy to grow.

Drawbacks

- Gender-Based Pricing: A significant drawback is the gender-based pricing, which results in higher costs for females due to longer life expectancy and higher usage rates.

- Cost Implications for Females: Women may face premiums that are 60-70% higher than those for men.

Tax Advantages and Funding Options

Traditional long term care insurance can be funded through Health Savings Accounts (HSAs) or Health Reimbursement Arrangements (HRAs), offering tax-free premiums. There are also potential tax deductions for self-employed individuals or small business owners.

For more information on other types of care insurance, you can explore Short Term Care Insurance and Hybrid Long Term Care Insurance.

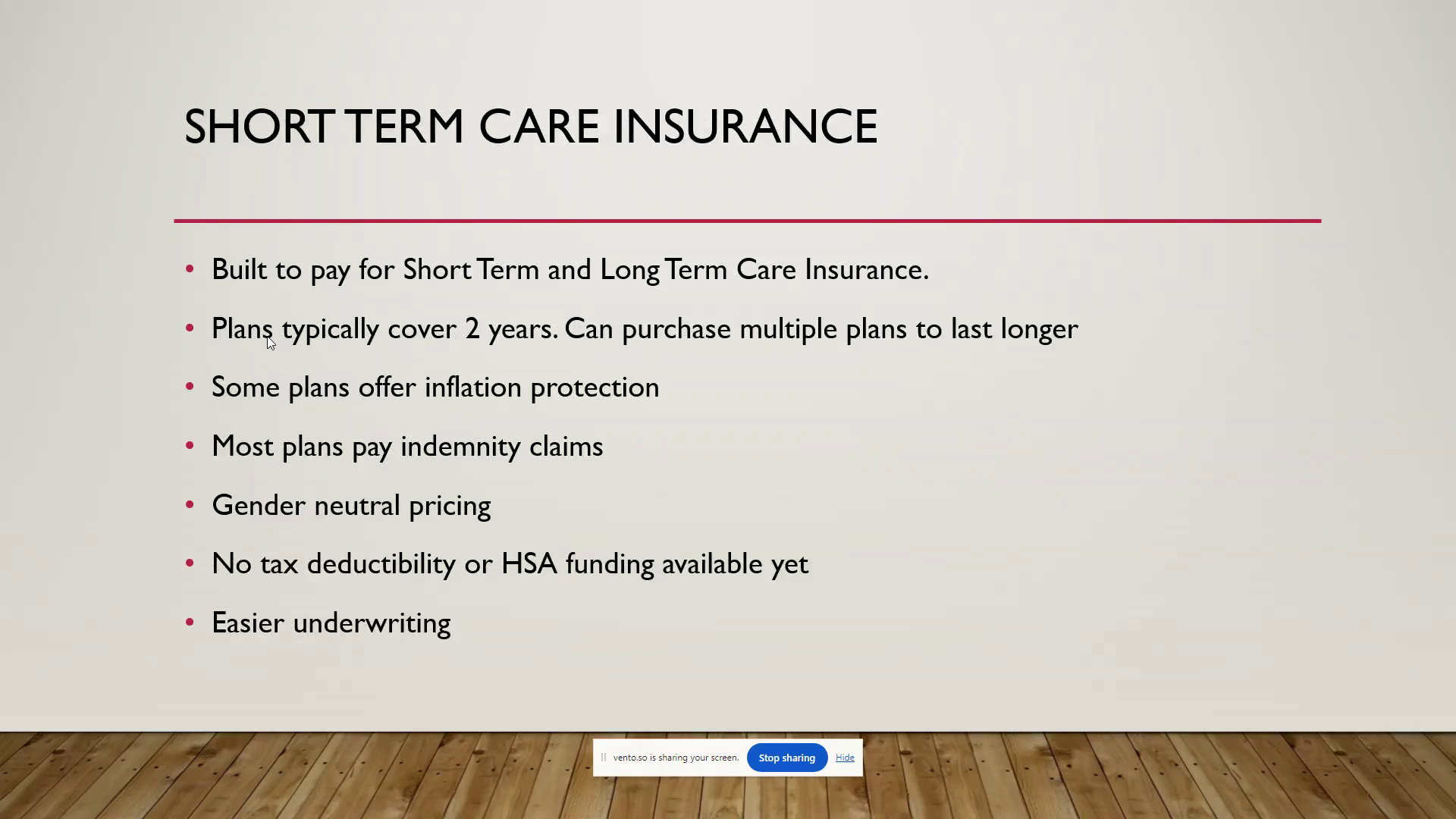

Short Term Care Insurance Overview

Short term care insurance is a rapidly growing option in the insurance market, designed to cover both short and long-term care needs. Despite being labeled as short term, these plans often resemble long-term care insurance in their structure and benefits.

Key Features

- Cost: Generally, less expensive than traditional Long Term Care Insurance and Hybrid products.

- Easy Underwriting: More accessible than traditional long-term care insurance, accepting a wider range of health conditions.

- Indemnity Payment Structure: Pays a fixed benefit amount, allowing any excess to be used flexibly, often tax-free.

- Gender-Neutral Pricing: Offers equal pricing for men and women, making it particularly appealing to females.

- Coverage Duration: It’s more about the dollar amount than the duration. Technically, this represents two years of coverage, but in most cases, it pays out more in benefits than it actually costs.

- Flexibility: Offers coverage for both physical and cognitive impairments without a minimum duration requirement.

Benefits

- Inflation Protection: Some plans offer this feature, though many opt for larger initial benefits instead.

- Flexibility in Care Providers: Pays you directly. Typically, the benefit is higher than the cost which will provide you with extra funds to pay who you want outside of licensed care providers.

Limitations

- Tax Benefits: While your benefits paid to you are tax-free. Currently your premiums lack tax deductibility and HSA funding options.

Conclusion

Short term care insurance is an attractive option for those seeking a cost-effective solution with significant benefits, especially for individuals who may not qualify for traditional long-term care insurance. It provides a flexible and accessible alternative, particularly for women and those with health issues.

For more information on related insurance options, see Traditional Long Term Care Insurance and Hybrid Long Term Care Insurance.

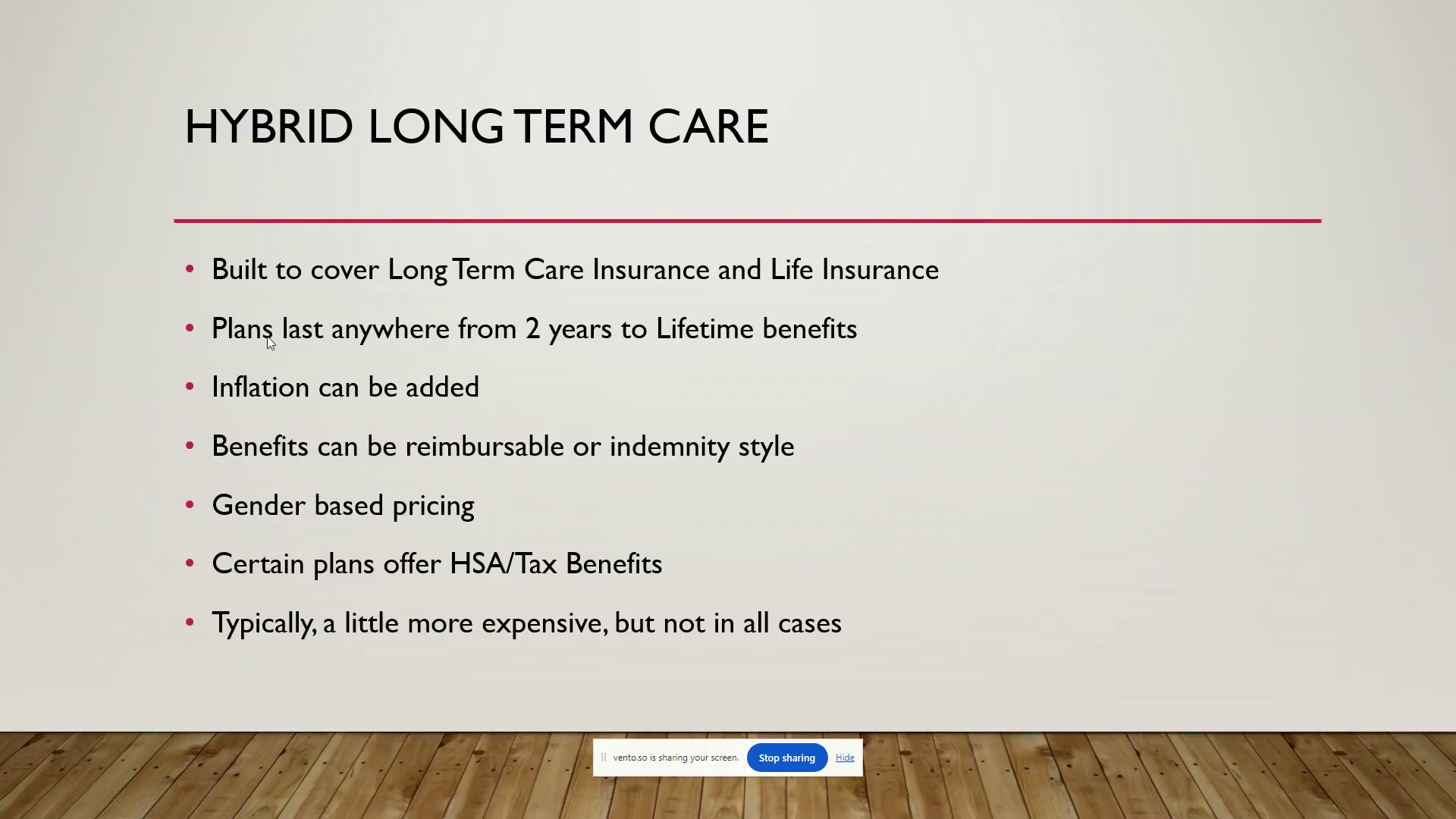

Hybrid Long Term Care Insurance

Hybrid long term care insurance is designed to combine the benefits of long term care and life insurance. This type of insurance is particularly appealing to those who are concerned about purchasing a policy they may never use. With hybrid plans, if long term care is not needed, the policyholder still benefits from a life insurance payout, often exceeding the premiums paid.

Key Features

- Coverage Duration: Plans can range from two years to lifetime benefits, depending on the carrier.

- Inflation Protection: Options to add inflation protection are available, though not as common as in traditional plans.

- Benefit Structure: Benefits can be either reimbursable or indemnity style, offering flexibility based on the carrier.

- Pricing: Gender-based pricing is applied, but it tends to be more balanced due to the combination of life insurance and long term care underwriting.

- Tax Benefits: Some plans allow funding through Health Savings Accounts (HSAs) or offer tax benefits for the long term care portion.

- Cost: Generally more expensive than other options, but not always, especially with paid-up options like ten-pay or single-pay plans.

Ideal Candidates

Hybrid plans are well-suited for:

- Couples and individuals under 60

- Those seeking a paid-up option to avoid payments during retirement

- Self-insurers who prefer a guaranteed benefit over savings

For more information on other types of care insurance, you can explore Traditional Long Term Care Insurance and Short Term Care Insurance.